The United States is currently in debt by over $39 trillion. When will this bill come due and why does it matter?

The United States owes money to its creditors in the form of US Treasuries - Bonds, Notes, and T-Bills. Much of this debt will have its principal due to be repaid and its balance rolled over into new securities in the near future. Other portions of this debt are due farther out, which we call long duration. When a long duration security such as a 30-year Treasury bond has been outstanding for a long time and the expiration date nears, it will trade more like a T-Bill, and colloquially may be referred to as such. T-Bill, Note, and Bond are simply classifications based on remaining time to maturity.

| Security Type | Term Length | Specific Maturities |

|---|---|---|

| Treasury Bills (T-Bills)[1] | Short-term | 4, 8, 13, 17, 26, or 52 weeks |

| Treasury Notes (T-Notes)[2] | Medium-term | 2, 3, 5, 7, or 10 years |

| Treasury Bonds (T-Bonds)[3] | Long-term | 20 or 30 years |

| Floating Rate Notes (FRNs)[4] | Medium-term | 2 years |

You can find the breakdown of when all current US debt is due in a publication called the Monthly Statement of the Public Debt (MSPD). Published on the fourth business day of each month, it details the U.S. government’s outstanding debt obligations as of the end of the prior month, including due dates, the statutory debt limit, and where Treasuries are held — using categories such as “debt held by the public” and “intragovernmental holdings.”

The duration of outstanding Treasuries matters. If a trillion dollars in short-term T-bills is set to mature in the near future, the Treasury must issue new debt to repay that principal. If that refinancing is done using long-term bonds, which may carry a significantly higher interest rate, it can increase the government’s overall interest burden. When deciding the duration mix of new securities to roll expiring debt into, the Treasury department must consider market conditions versus the government’s need to pay a stable, manageable interest rate over the long term.

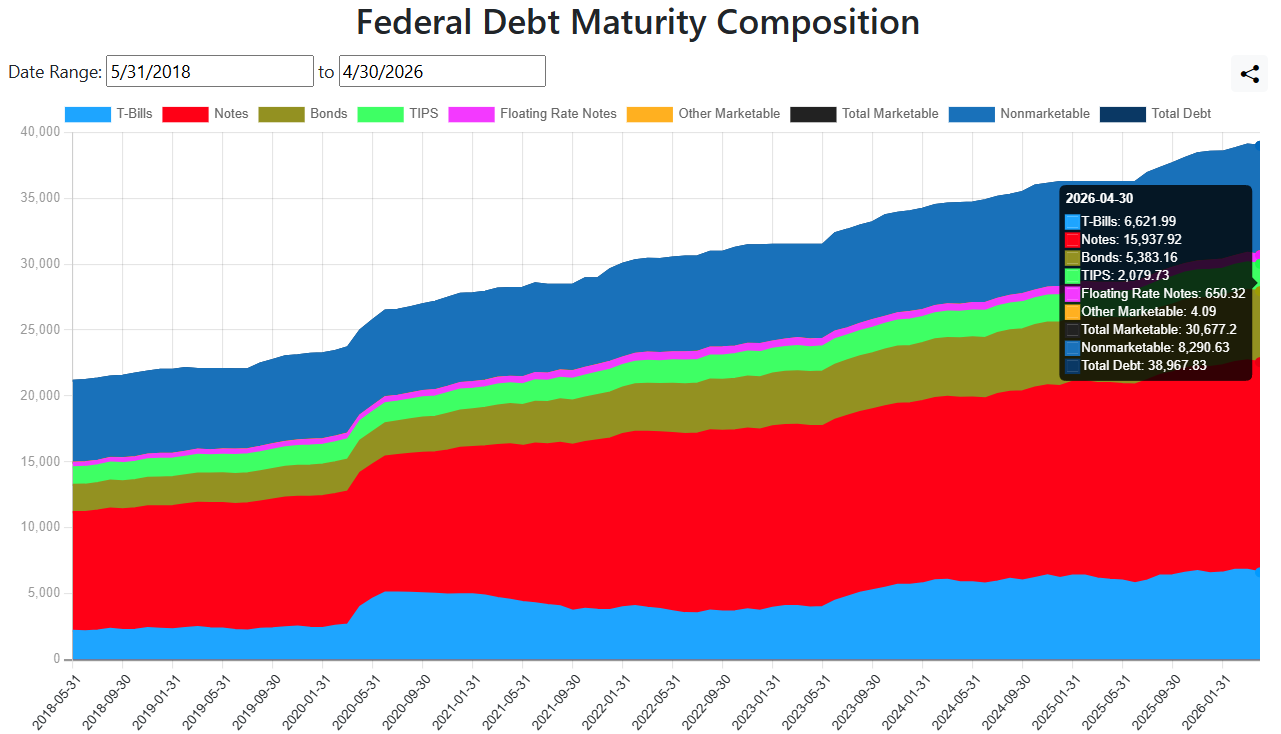

On this website’s Federal Debt Maturity Composition page, you can find a visual representation of the MSPD report. This chart breaks down the total US debt by the categories provided by the US government, allowing you to easily compare the size of each grouping of debt and how they have changed over time. In addition to the familiar categories of T-Bills, Notes, and Bonds, some of the reported categories are more ambiguous on the time frame they are due. Treasury Inflation-Protected Securities (TIPS) can be issued in durations of 5, 10, or 30 years, and are aggregated into a single category. However, they comprise less than 6% of the total US debt. Roughly 21% of the debt is in nonmarketable securities - illiquid bonds which include the Series EE and I savings bonds held by individuals[5], State and Local Government Series Securities[6], and certain issues meant to be held in intra-governmental accounts[7].

The debt aggregation charts on this website are based on information obtained from the FiscalData website managed by the US Treasury Department. There you can download the source data sets and the full PDF publication of the MSPD.

The MSPD also contains much more granular data, which can be used to make even more detailed breakdown charts. If this is of interest to you, please come on our Patreon and provide your feedback and feature requests!

- TreasuryDirect.gov - Treasury Bills

- TreasuryDirect.gov - Treasury Notes

- TreasuryDirect.gov - Treasury Bonds

- TreasuryDirect.gov - Floating Rate Notes (FRNs)

- Series EE and Series I US savings bonds held by individuals

- State and Local Government Series Securities

- https://www.federalreserve.gov/econresdata/notes/feds-notes/2015/federal-debt-in-the-financial-accounts-of-the-united-states-20151008.html